EU Taxonomy

A framework for true sustainability

How Siemens masters the EU taxonomy with hfp

In less than a year, we developed and implemented the company-wide EU taxonomy management system for Siemens AG on the basis of our no-code platform. It takes over the task of technical assessment in the corporate reporting process. The product, project and service portfolios as well as relevant locations and suppliers of Siemens AG worldwide are assessed in terms of eligibility and alignment and the associated sales, operating costs and investments are recognised in the annual financial statements on this basis. For the first time, Siemens AG successfully carried out its EU taxonomy reporting for fiscal year 2023 using our software system.

ASSESSMENT SYSTEM

What is the EU taxonomy?

With the European Green Deal, the 27 EU member states are aiming to transition to a modern, resource-efficient and climate-neutral economy by 2050. In order to promote this transformation process through private investment in sustainable companies, the EU taxonomy was created as a separate assessment tool for the sustainability of economic activities. As a result, companies are obliged to assess their individual value creation processes with regard to the environmental targets defined by the EU and to report publicly on their progress in this regard. Companies are faced with the following challenges:

THOROUGH ANALYSIS

Objectives of the EU taxonomy

The EU Taxonomy is a subset of the CSRD and sets out a large number of detailed criteria against which companies must assess their activities. Starting with the 6 environmental objectives, also known as EU Taxonomy Goals, of the EU Taxonomy Regulation, through more than 100 business activities that are considered taxonomy-compliant, to extensive criteria that must be met so that the company's activities do not cause significant damage to other environmental objectives (DNSH Criteria Check). This requires a deep understanding of the requirements and a careful analysis of your own business processes. Due to the high level of complexity and the extensive reporting requirements, the use of EU taxonomy software is particularly worthwhile for larger companies.

NEW REQUIREMENTS

Data availability and quality

The EU taxonomy requires a large number of detailed key figures. Many key figures and assessments. The particular challenge here lies in the fact that the analysis involves non-financial key figures that have not yet been collected and processed in a structured manner in the vast majority of companies. For example, it is necessary to know the material composition of individual products, to measure GHG emissions during production or to analyze the impact of climate change on individual areas of the company. This makes it necessary to adapt internal processes, procedures and IT systems, create new control mechanisms and involve numerous stakeholders in the new requirements. processes. The deadlines for this are short.

EU TAXONOMY REPORTING OBLIGATION

Timeline for implementation

Since 2022, companies that are obliged under the NFRD have had to report on the EU taxonomy. As the regulations in previous years only defined the first two environmental objectives in more detail, the reporting obligations were manageable in the past. This will change for large, capital market-oriented companies with 500 or more employees with the successor regulation CSRD and the 2024 financial year (report in 2025). For this reporting year, it is not only mandatory to report on taxonomy eligibility for all six environmental objectives, but also to check taxonomy alignment for the first two environmental objectives. The assessment of taxonomy conformity in particular significantly increases complexity due to the DNSH assessment for all six environmental objectives. From 2025, the EU taxonomy reporting obligation will also be extended to smaller companies.

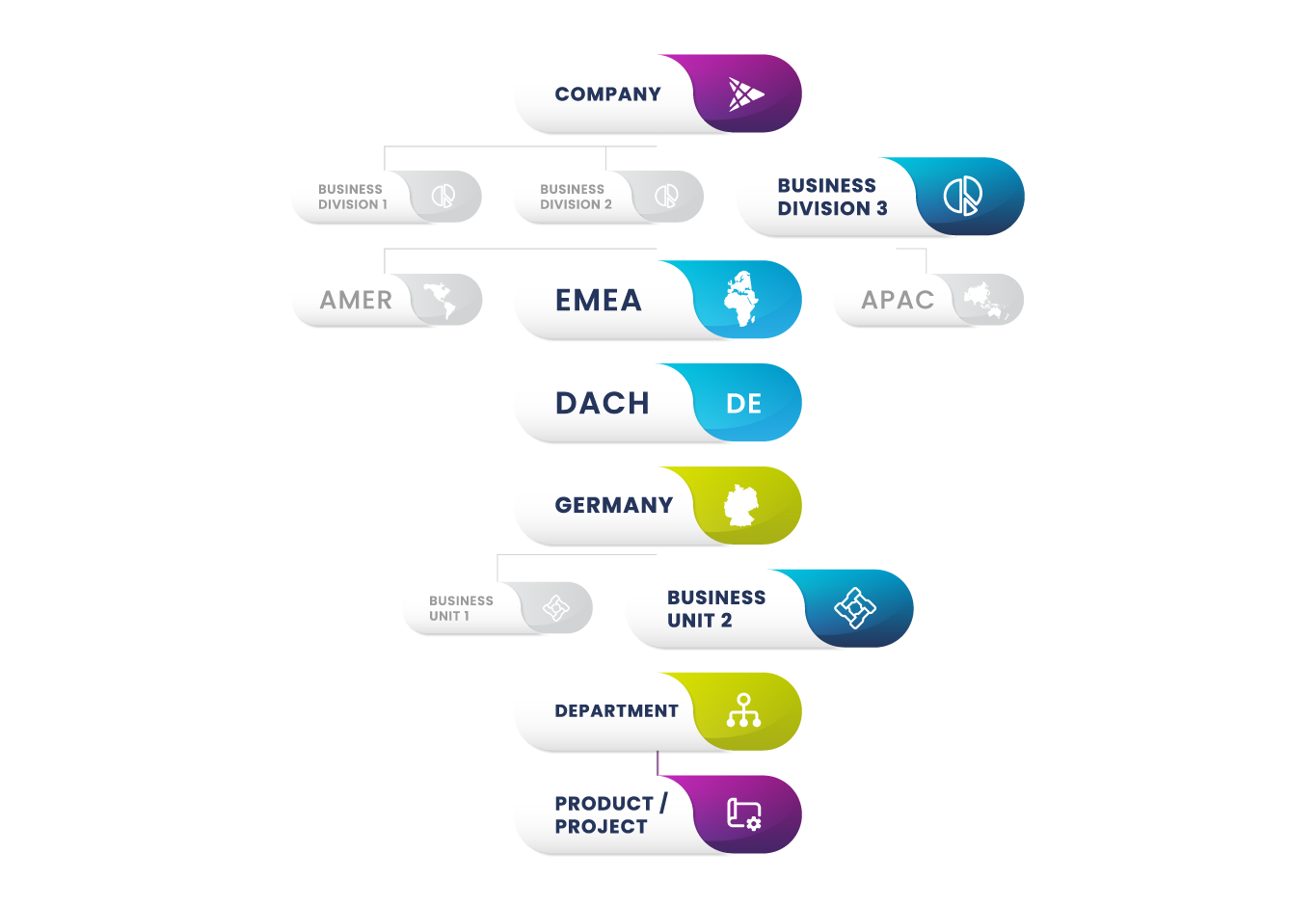

1. Your corporate structure - fully mapped

Your corporate structure mapped in hfp Impact Manager allows for high-level EU Taxonomy compliance checks, with results cascading down to all subordinate levels, saving thousands of individual verifications. Yet, you maintain flexibility to make specific adjustments or conduct additional checks at any detail level on any object.

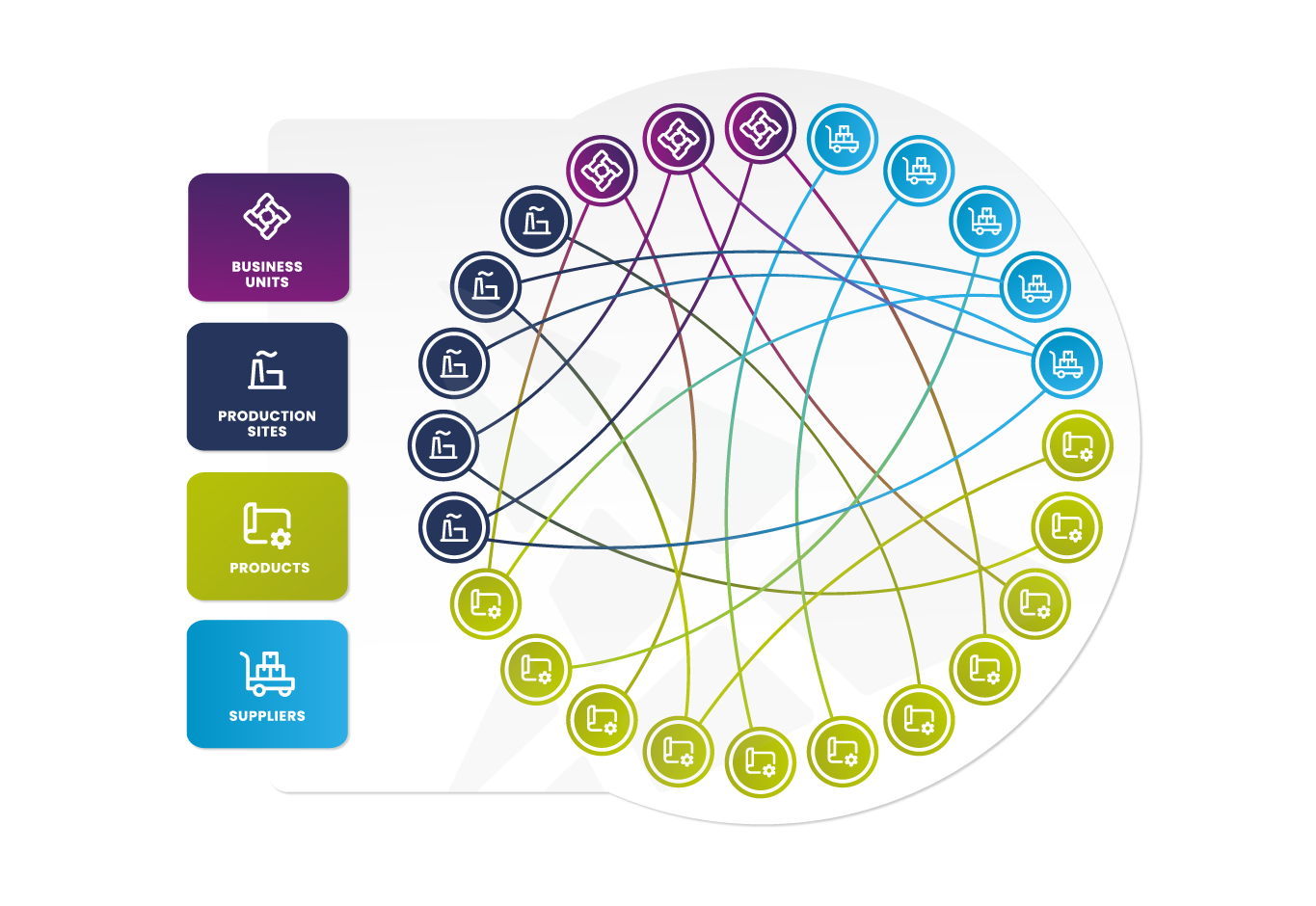

2. Audit efficiency through n:m relationships

Thanks to our relational data model, hfp Impact Manager can map n:m relationships between all objects. This means you only need to audit suppliers and production sites once, and the results are automatically applied to all connected products and areas. hfp Impact Manager appropriately allocates your revenue and demonstrates in detailed reports the impact of compliant suppliers or production sites. Thus, we can distinguish between revenue, CapEx, and OpEx that are non-eligible, eligible, and aligned - even within a specific product or project and show you possible ways of optimization.

3. Collaboration - simultaneous Group-wide assessment

hfp Impact Manager facilitates seamless collaboration across divisions and functions. Comprehensive role and rights management ensures that your employees only see the organizational parts and audit steps relevant to them, enabling you to assign audit tasks with precision. This allows for smooth, worldwide, cross-functional cooperation in your EU Taxonomy audits.

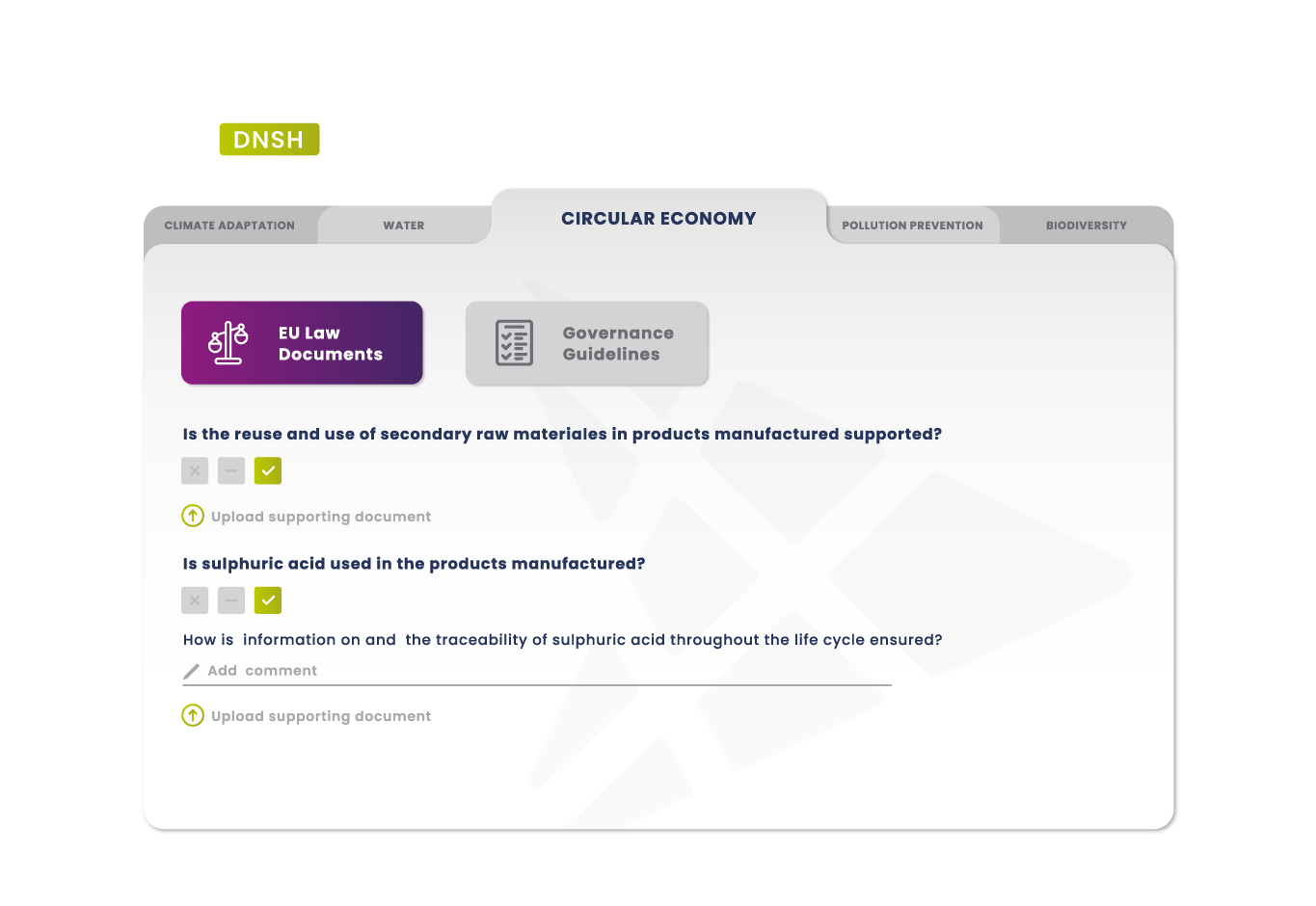

4. Context-sensitive audit workflow

The EU Taxonomy is complex - our system aids you with a context-sensitive audit workflow, allowing you to navigate only the relevant section of the regulation through a well-structured audit cascade. From selected Eligible Activities for each business division and product group, through substantial contribution, to the DNSH criteria assessment. Your auditors are presented with only the pertinent criteria and questions at each step. The audit steps are logically sequenced so that given answers determine the subsequent questions, guiding you precisely through the process to the audit's conclusion.

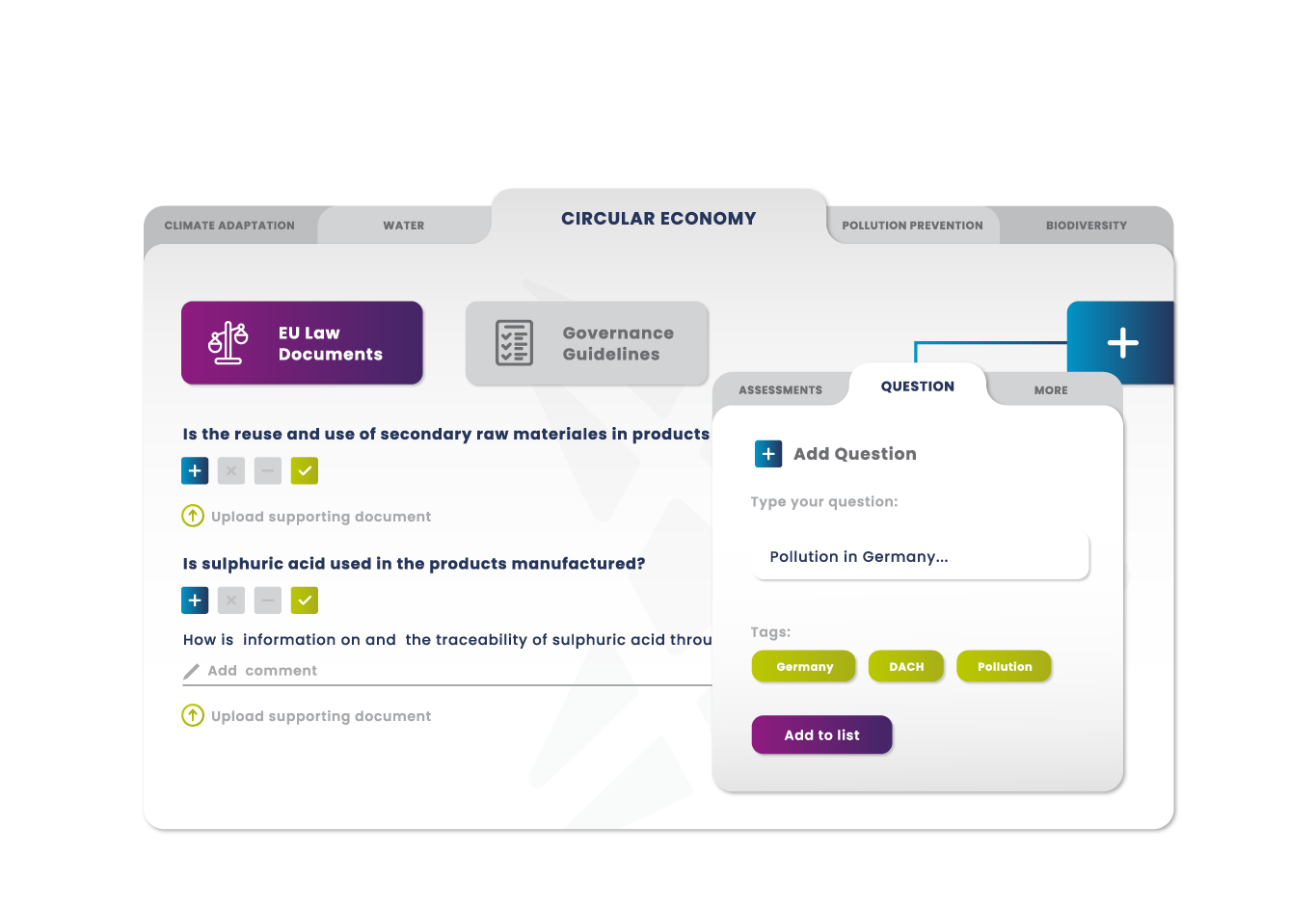

5. Standard if possible - customised where necessary

hfp Impact Manager incorporates EU Taxonomy standards and, through its no-code configuration and customizable instance, offers complete flexibility at the same time. Do you have specific acceptance and audit criteria for eligibility or alignment? Does the audit need to adhere to the four-eyes principle? Have you established individual evidence and audit steps for certain DNSH criteria? - hfp Impact Manager effortlessly and individually maps all this by configuration.

6. Seamless IT integration

hfp Impact Manager seamlessly integrates into your existing IT infrastructure, whether operated on-premise, virtualized, or in your private or public cloud. With hfp Impact Manager, you can capture, audit, and report all ESG and EU Taxonomy data from a central location. It connects to your current IT infrastructure via APIs and ETL processes without requiring changes to your existing systems. We leverage our pre-existing interfaces with common systems like SAP, Snowflake, or OIDC, as well as custom API connections tailored to your needs. Reporting and raw data are delivered back to your systems for further processing in any required level of granularity and format (API call, CSV, XML, PDF, etc.).

CONTACT US TODAY

Learn more about EU Taxonomy

We look forward to getting to know you in an initial meeting to see how we can best support you - free of charge and without obligation! Simply use our contact form.